The retirement story nobody tells you

There's a five-layer income system that's generating $8,000 to $12,000 per month for a small group of high-net-worth retirees. It's based on what Ray Dalio calls the Holy Grail of investing. And if you have at least $500,000 saved for retirement, it's worth understanding before you make decisions you can't unwind.

But first, the part most retirement research skips:

Why the strategy you've spent forty years following is about to stop working, and is probably already costing you more than you realize.

Most people picture retirement as a number. A million dollars. Two million. Whatever the calculator on Vanguard or Fidelity told them they needed to "be safe."

So they spend forty years chasing it. They max out the 401(k) with all their matches. They contribute to the IRA. They pick the target-date fund. They follow the rules.

And then, finally, they hit it.

The number on the statement looks the way they pictured it. The mortgage is paid off. And they are finally done.

But when it's time to actually live and fulfill all the retirement dreams they realize that the instruments at their disposal will not give them what they pictured.

There's a reason most retirement guides leave you with more questions than answers, they're written for everyone, which means they're built for no one. What follows is the framework the wealthiest retirees actually use, broken down so you can evaluate whether it makes sense for your situation.

The two retirees who learned this the expensive way

Trina is a retirement YouTuber. She had about $500,000 saved. She'd done everything the conventional wisdom said to do, didn't try to time the market and maxed out her 401(k).

She decided to plan on her own.

Then she discovered the truth that made her sick to her stomach.

"I made a $235,000 mistake with my retirement money," she said in a video that's now been viewed over a million times. "And the worst part? Nobody told me otherwise. I didn't use a financial planner."

$235,000 isn't a typo. That's the difference between the retirement most people have and a well-planned retirement.

Duane is another retirement YouTuber. He had a similar amount saved, about $500,000, and ran into a different version of the same problem. By his own estimate, his DIY approach cost him somewhere between $40,000 and $50,000 in returns he should have captured but didn't.

"I wasted two, three years and I would probably be forty, fifty thousand dollars at least better now in my retirement savings if I didn't."

These are not unsophisticated people. In fact, they are 'retirement YouTubers' who spend a lot of time doing due diligence about retirement. They're diligent savers who did everything right by the rules they were given, and the rules turned out to be incomplete.

The question that should bother you isn't "how did this happen to them?"

It's "how would I know if it was happening to me?"

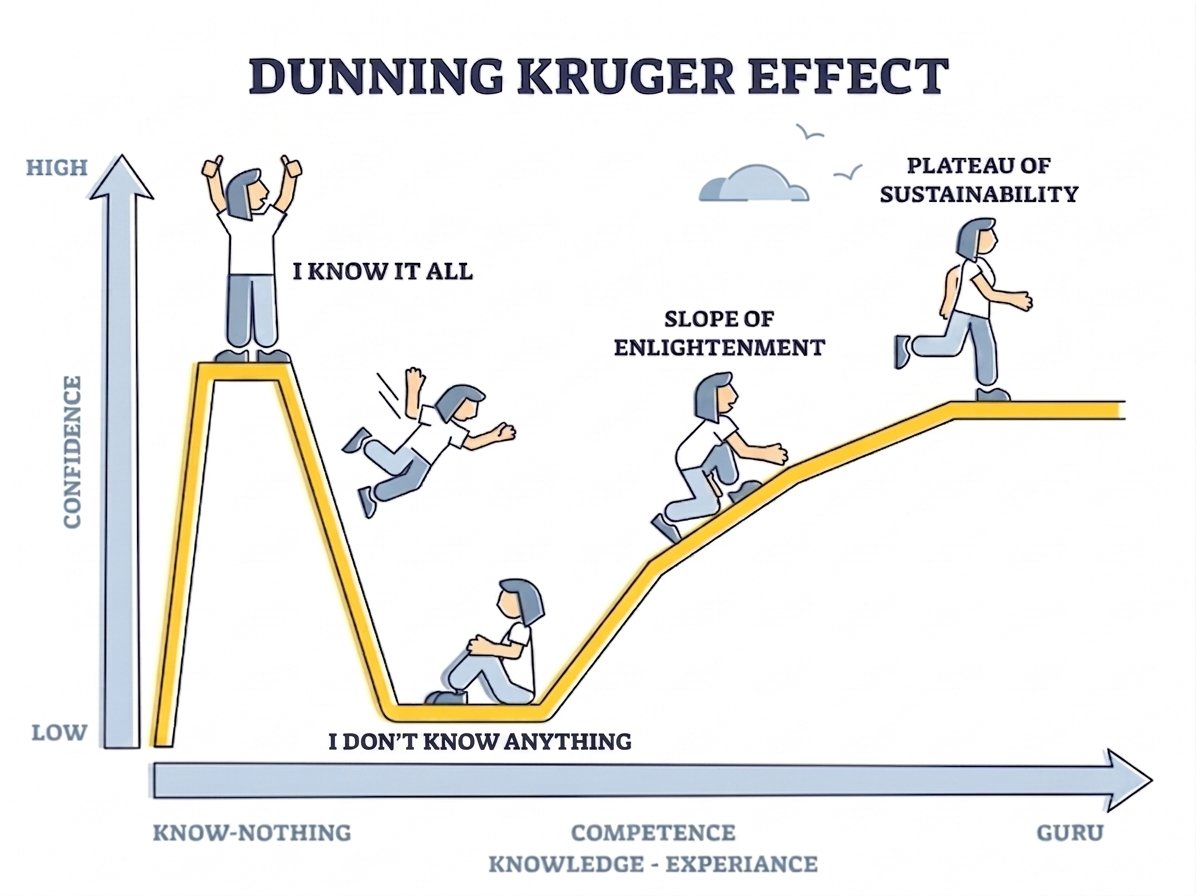

I came across an article entitled The Dunning-Kruger Effect.

And that's exactly what was happening to Duane and Trina, it wasn't that they weren't smart or that they didn't mean well. It was simply what can be described in one quote:

"You don't know, what you don't know"

And some years into retirement it just left them with a "If I had only known…"

Why "growth" and "income" are not the same problem

Here's the part most people miss until it's too late:

The skill of growing a portfolio over thirty years is almost completely different from the skill of converting a portfolio into reliable monthly income for the next thirty years.

A different phase requires a different portfolio. And the two pieces of advice that almost every American retiree has been handed for the income phase, the 4% rule and the 60/40 portfolio, are both not going to cut it and will force retirees to downgrade their lifestyle.

The 4% rule was developed in the early 1990s by a financial advisor named William Bengen. The idea: withdraw about 4% of your portfolio each year and you can reasonably expect not to run out. Bengen himself has now said publicly, more than once, that the rule is no longer the right framework for most modern retirees. Interest rates have changed. Inflation has changed. Lifespans have changed. The tax landscape has changed. But also financial instruments have changed.

And it shows. A 4% withdrawal on a $1 million portfolio is about $3,300 a month before taxes. Most retirees with that level of savings need two to three times that to live the way they pictured. So the rule quietly condemns you to a shrinking lifestyle: cutting back, saying no, watching inflation eat your purchasing power year after year. You spent forty years building wealth so you could spend the second half saying no to things?

The 60/40 portfolio, 60% stocks, 40% bonds, has its own problem. Barron's, the Wall Street Journal, and CNBC have all run versions of the same headline in the last few years: the 60/40 is dead. The premise of the strategy was that bonds would zig when stocks zagged, smoothing out your ride. That premise has stopped holding up. Stocks and bonds have moved together too often for the strategy to do its job, and a "conservative" $1 million portfolio built this way has at times lost over $200,000 in a matter of months.

The retirees this article is about figured this out, often the hard way, and decided to build something different.

What "different" actually looks like: the layered income approach

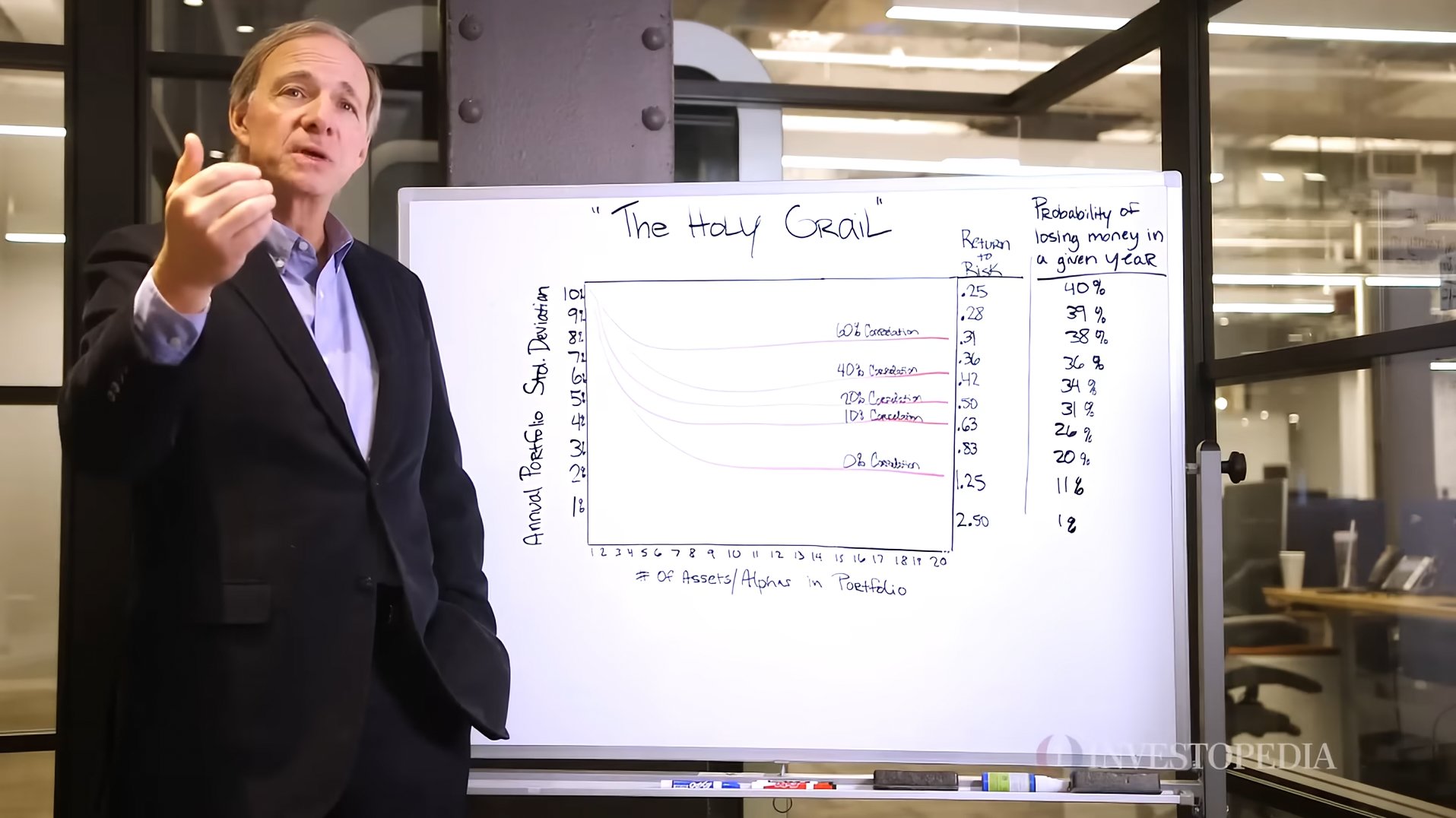

The strategy goes by different names in different corners of the wealth management world. Some call it "income stacking." The most rigorous version of the underlying idea was popularized by Ray Dalio, the founder of Bridgewater Associates, who calls it the Holy Grail of investing: building a portfolio out of streams of return that don't all move in the same direction at the same time.

In retirement income planning, that idea gets translated into something called a layered income portfolio.

Instead of putting most of your money into one or two big buckets, typically stocks and bonds, and then withdrawing from the whole pile, you build five separate layers, each engineered for a different job. When one layer underperforms, the others keep paying. There's no single point of failure.

The five layers, in plain language:

Layer one, the foundation. Your stable baseline income. Designed to deliver steady, predictable payments through normal market conditions. This is the layer that pays your bills regardless of what the headlines are doing.

Layer two, the volatility shield. Specifically engineered to generate income during market downturns, not in spite of them. While most portfolios bleed during chaos, this layer is structured to keep producing.

Layer three, the inflation hedge. When the dollar weakens and prices rise, this layer adjusts upward. It exists to protect your purchasing power over a 20- or 30-year retirement, not just your nominal account balance.

Layer four, the tax optimizer. This is where most of the long-term value gets created or destroyed. Built for maximum tax efficiency: minimizing what the IRS takes from your retirement income each year, and ensuring more of what's left passes to your heirs rather than to estate taxes.

Layer five, the guarantee. Income that keeps coming no matter what happens to markets, banks, or the economy. Social Security and pensions live here, but for high-net-worth retirees this layer also includes specific guaranteed instruments most people don't have access to.

When advisors talk about "income engineering" rather than "investing," this is what they mean. The portfolio isn't designed to maximize one number. It's designed to do five different jobs at once, with no single one capable of bringing the whole thing down.

The tax layer is where most of the money lives

Of the five layers, one of them tends to make a bigger dollar difference over a 20- or 30-year retirement than the other four combined: the tax layer.

This isn't because taxes are exotic or complicated. It's because the tax structure of a typical American retiree's accounts is almost perfectly designed to maximize what the IRS collects from them.

The traditional path looks like this: contribute pre-tax to a 401(k) for thirty years. Watch it grow. Roll it into an IRA at retirement. Begin drawing from it. Pay ordinary income tax on every dollar that comes out. Get pushed into a higher tax bracket when Required Minimum Distributions start at age 73. Pay even more.

That's the default. It's what happens if you do nothing differently.

But there's so many instruments like tax loss harvesting, tax lot selling, staying under capital gains cliffs, and strategic Roth withdrawals. All while avoiding the traps that trip up most retirees, things like wash sale rules and IRMAA thresholds. Vanguard research shows that only one out of those, tax-loss harvesting can add over 100 basis points (1%+) of potential "tax alpha" annually for investors, and particularly more when using direct indexing or proactive management.

The portfolio sizes can be identical. The lifetime tax bills end up wildly different, and the difference, in many cases, is bigger than the difference between a good portfolio return and a great one.

This is one of the reasons the strategy used to be reserved for the ultra-wealthy. The combination of advanced tax planning, institutional investment access, and customized portfolio construction was something you could only get if you wrote a big enough check to the right private wealth firm in the right zip code.

That has started to change.

Who this is actually for, and why most people will never see it

There's a version of this story that ends with "and you can do this yourself if you just read the right book." That version is wrong.

The reason these strategies have historically been gated isn't a conspiracy. It's that building a layered income portfolio with proper tax structuring requires three things most people don't have access to as individuals:

Institutional-grade investment access. Private credit funds, structured income vehicles, and certain tax-efficient instruments are not available through retail brokerages. They're not on Schwab or Fidelity who just want your portfolio to stay on their platforms so their fees grow. They require relationships that take years and minimum check sizes to establish.

Coordinated tax and estate planning. A good retirement income plan touches your tax return, your estate plan, your insurance, your Social Security election, your Medicare planning, and your charitable strategy, all at once. Most financial advisors specialize in one or two of these, not all of them.

Time. Building this kind of plan well takes 15–40 hours of professional work upfront, plus ongoing rebalancing and tax-strategy updates as the law and your life change.

For most of recent history, this meant the strategy was only practical for retirees with $5 million or more, enough to justify the fees of a traditional private wealth advisor.

What changed in the last few years is that a small group of these advisors, working under what's sometimes called the virtual wealth office model, started accepting clients nationwide using secure video meetings instead of in-person appointments. The geographic restriction disappeared. The minimum dropped to $500,000 in investable assets. And the cost structure shifted from "high fixed fees" to "performance-based" arrangements where the client sees the entire plan before paying anything.

This isn't for everyone. It's not appropriate for someone with $50,000 saved who needs to focus on building a foundation first and where 401(k)s are the correct path. It's not appropriate for someone with $50 million who already has a multi-generational family office running things. It's specifically built for the band of retirees in the middle, that were forgotten before, the ones who have done the work to save real money, but who haven't yet had access to the kind of structured income planning that the wealthy take for granted.

What other retirees in this band have actually done with it

A few examples, with names changed where requested:

Mark and Ellie had $1.3 million in taxable brokerage accounts and were able to retire early at 45, generating $12,000 per month, a $2,000 cushion above the dream income they'd retired to hit.

John, an attorney with $2 million saved, generates $16,000 per month on top of what he was already getting from Social Security, and won't need to do a single withdrawal from his principal.

James, a recently divorced retiree, thought it'd be tough to live well with the ~$815,000 net worth he was left with. He'd have been happy with "enough" to cover bills. After tightening up how his retirement income streams were set up, he's now bringing in $9,000+ per month.

These are not investment "wins" in the conventional sense. None of these people picked a hot stock or got lucky on a market call. What they did was rebuild the structure of their income so that their existing assets work harder and more predictably.

Taking the same dollars and putting them through a more deliberate plan.

The conversation worth having

If you've made it this far, you probably fall into one of two camps.

You either already have a clear, written, tax-optimized retirement income plan that does most of what's described above, in which case this research is a useful confirmation that you're on the right track, and you don't need to do anything.

Or you don't.

If you don't, the most useful next step isn't to try to build one yourself from a guide. It's to have a direct conversation with someone who builds these plans for a living, and see, for your specific situation, your specific accounts, your specific tax picture, what the structure could actually look like.

The wealth advisors who work in this niche have set up a free consultation process specifically for retirees evaluating whether this approach makes sense for them. There's no obligation to engage further. They build out a draft of what your plan could look like before any decision to work together. If their plan isn't measurably better than your current setup, you walk away with their analysis at no cost.

If that sounds useful, the link below will check current availability for the specialized advisors who handle income-layered retirement plans. If your situation fits, you'll see open times within the next two to three weeks.

A final note

Most retirement advice is written to make you feel one of two things: scared enough to do something drastic, or comfortable enough to do nothing.

The truth is usually in the middle. A retirement portfolio that's been well-saved but never been structured for income is just incomplete.

That's the conversation worth having before you take your first major withdrawal, not after.